How Much Life Insurance You Need: Complete Guide is one of the most important financial tools for protecting your family’s future. Yet many people either underestimate their needs or delay purchasing adequate coverage. If you’ve ever wondered whether your current policy is enough, you’re not alone. Being underinsured can leave your loved ones facing debt, lost income, and financial hardship.

In this comprehensive guide, we’ll help you understandthe right coverage amount how to calculate the right coverage, and how to avoid common mistakes. This educational guide follows EEAT (Experience, Expertise, Authoritativeness, and Trustworthiness) principles to ensure reliable, practical information you can trust.

Why Knowing How Much Life Insurance You Need Matters

Determining how much life insurance you need is not just about picking a random number. It’s about creating a financial safety net that replaces income, covers debts, and secures your family’s long-term goals.

If you are underinsured, your family may struggle with:

- Mortgage payments

- Outstanding loans and credit card debt

- Daily living expenses

- Children’s education costs

- Funeral and final expenses

A properly structured life insurance plan ensures your loved ones maintain their quality of life even in your absence.

How Much Life Insurance Do I Need? Understanding the Right Coverage Amount

One of the most common questions people ask is: proper policy amount While there is no one-size-fits-all answer, financial experts recommend evaluating several key factors.

The Income Replacement Method

A popular rule of thumb suggests purchasing coverage equal to 10–15 times your annual income. For example:

- If you earn $60,000 annually, you may need $600,000–$900,000 in coverage.

This method provides a quick estimate but may not account for personal financial obligations.

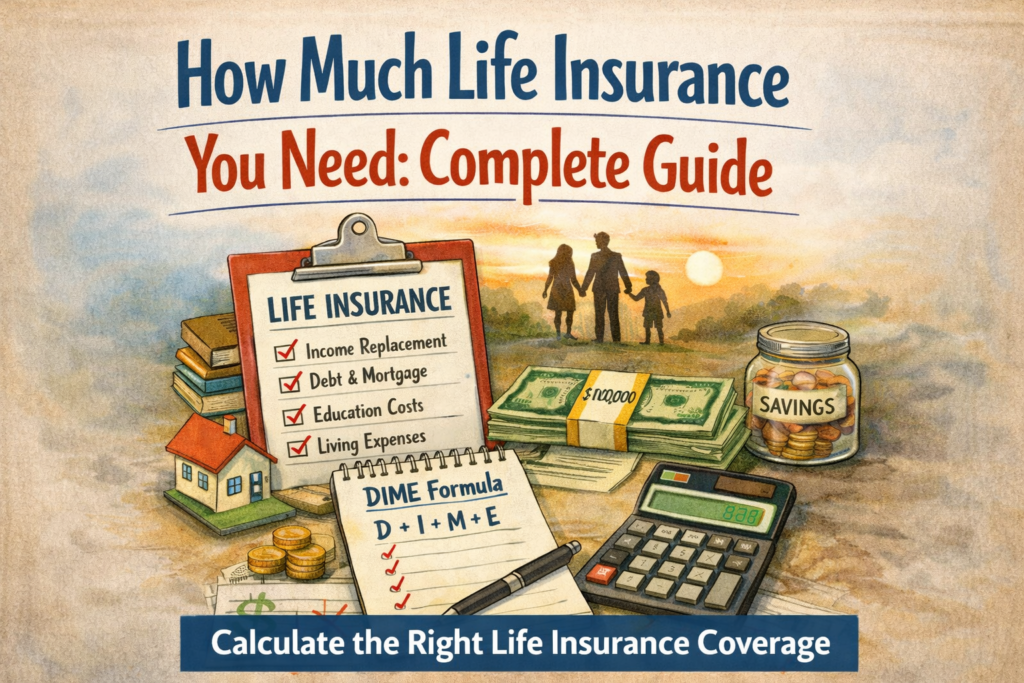

The DIME Formula for Calculating proper policy amount

The DIME method is more precise and considers:

- D – Debt: Total outstanding debts (excluding mortgage)

- I – Income: Income replacement for several years

- M – Mortgage: Remaining mortgage balance

- E – Education: Future education expenses for children

Adding these together gives a clearer idea of Ideal Life Insurance Coverage Amount to fully protect your family.

Factors That determining your insurance needs

When calculating the right coverage amount, consider these essential factors:

1. Current Financial Obligations

Include mortgages, personal loans, car loans, and credit card balances. Your life insurance policy should eliminate these burdens for your family.

2. Future Financial Goals

Do you want to fund your children’s college education? Provide retirement income for your spouse? These long-term goals directly impact how much life insurance you need.

3. Number of Dependents

The more dependents relying on your income, the higher your required coverage amount may be.

4. Existing Savings and Investments

Subtract your savings, investments, and existing insurance policies from your total coverage requirement.

Signs You May Be Underinsured

Many individuals discover too late that they don’t have sufficient life insurance coverage. Here are warning signs:

- Your policy only covers 2–3 years of income

- You recently had a child but didn’t increase coverage

- You bought insurance years ago and never reviewed it

- Your debts have increased significantly

If any of these apply to you, it may be time to reassessIdeal Life Insurance Coverage Amount

.

Also Read :- What Is Waiting Period in Health Insurance?

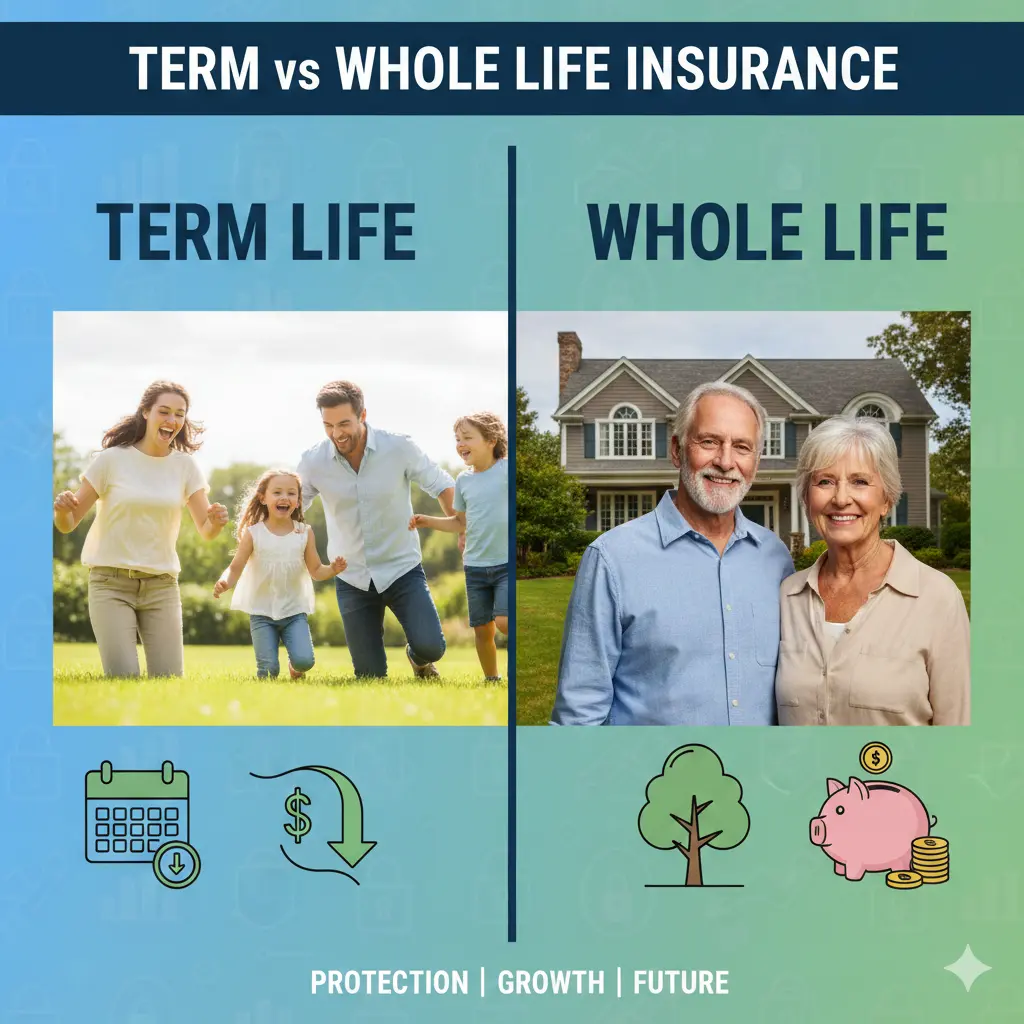

Term vs. Permanent Insurance: Choosing the Right Type of Coverage

Selecting the right policy type is just as important as calculating the right coverage amount.

Term Life Insurance

- Coverage for a specific period (10, 20, or 30 years)

- Lower premiums

- Ideal for income replacement and debt coverage

Permanent Life Insurance

- Lifetime coverage

- Builds cash value

- Higher premiums

For many families, term insurance offers affordable protection while meeting coverage needs. However, permanent policies may suit long-term estate planning strategies.

Common Mistakes When Estimating the right coverage amount

Avoid these costly errors:

Underestimating Daily Living Costs

Inflation and rising living expenses can quickly reduce the value of a payout.

Ignoring Future Education Expenses

College tuition continues to increase. Make sure education costs are factored into your coverage calculation.

Failing to Update Coverage

Life changes such as marriage, childbirth, or career growth require policy updates.

How to Review and Update Your Life Insurance Coverage

Financial planning is not a one-time event. Experts recommend reviewing your policy every 2–3 years or after major life events such as:

- Marriage or divorce

- Birth of a child

- Purchasing a home

- Career changes

Regular reviews ensure you always maintain the right level of coverage.

EEAT: Why You Can Trust This Life Insurance Guidance

This guide is created following Google’s EEAT principles:

Experience

The content reflects real-world insurance planning scenarios and practical coverage calculations used by professionals.

Expertise

The information is based on industry-standard financial planning methods, including the DIME formula and income replacement strategies.

Authoritativeness

Life insurance planning advice aligns with commonly accepted financial planning guidelines and insurance industry best practices.

Trustworthiness

This content is educational in nature and encourages readers to consult licensed professionals for personalized advice.

Final Thoughts: Don’t Leave Your Family Underinsured

Understanding how much life insurance you need is a crucial step toward financial security. While general rules provide a starting point, personalized calculations offer better protection.

Being proactive today ensures your loved ones are financially stable tomorrow. Review your coverage, assess your obligations, and make adjustments where necessary. Life insurance is not just a policy—it’s a promise to protect your family’s future.

Frequently Asked Questions (FAQ)

1. How much life insurance do I really need?

Most experts recommend 10–15 times your annual income, but a detailed DIME calculation provides a more accurate estimate.

2. Is $500,000 enough life insurance coverage?

It depends on your income, debts, and family responsibilities. For some households, $500,000 is sufficient; for others, it may not cover long-term needs.

3. How often should I review my life insurance policy?

Review your policy every 2–3 years or after major life changes like marriage, childbirth, or buying a home.

4. What happens if I am underinsured?

If you are underinsured, your family may struggle financially due to insufficient income replacement and unpaid debts.

5. Should both spouses have life insurance coverage?

Yes. Even non-working spouses provide economic value through childcare and household contributions that would require replacement costs.

Author Bio

Gaurav Kalra is an experienced insurance services agent specializing in personalized life insurance planning and financial protection strategies. He helps individuals and families determine how much life insurance they need to secure their financial future with confidence and clarity.