Table of Contents

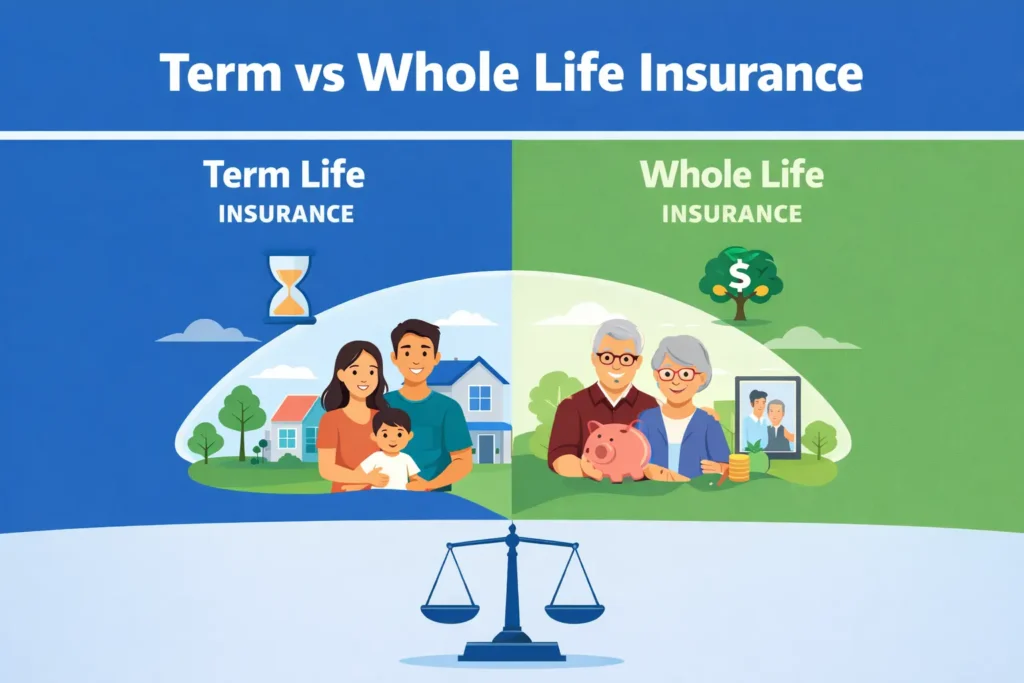

Choosing the right life insurance can feel confusing, especially when you’re stuck between two popular options: term life and whole life insurance. The debate of Term vs Whole Life isn’t about which is better overall—it’s about which fits your age, income, responsibilities, and future goals.

In this guide, we’ll break down the differences, explain which option suits each life stage, and help you make a confident, informed choice.

What Is Term Life Insurance?

Term life insurance provides coverage for a specific period—usually 10, 20, or 30 years. If the insured person passes away during that term, the beneficiary receives a payout. If the term ends and you’re still alive, the policy expires unless you renew it.

Key Features:

- Lower premiums

- Fixed coverage period

- No cash value

- Simple and affordable

Term life is ideal for people who want high coverage at low cost, especially during financially demanding years.

What Is Whole Life Insurance?

Whole life insurance offers lifetime coverage as long as you pay your premiums. It also includes a cash value component that grows over time and can be borrowed against.

Key Features:

- Lifetime protection

- Higher premiums

- Builds cash value

- Can act as a financial asset

Whole life works well for people who want permanent coverage and long-term financial planning benefits.

Term vs Whole Life Insurance: Core Differences

| Feature | Term Life | Whole Life |

|---|---|---|

| Coverage Length | Fixed term (10–30 years) | Lifetime |

| Premium Cost | Low | High |

| Cash Value | No | Yes |

| Flexibility | High | Moderate |

| Best For | Temporary needs | Long-term planning |

Understanding Term vs Whole Life starts with knowing what you need most: affordability now or financial stability for life.

Best Life Insurance by Age Group

In Your 20s

At this stage, you may have:

- Student loans

- Entry-level income

- Few dependents

Best Choice: Term Life

Low cost lets you lock in cheap rates while you’re healthy. Term life protects your family from debt if something happens unexpectedly.

In Your 30s

You might have:

- A mortgage

- Kids

- Growing income

Best Choice: Mostly Term Life, Sometimes a Mix

This is a critical time in the Term vs Whole Life Insurance decision. Term life covers major responsibilities, while a small whole life policy can start building long-term value.

In Your 40s

You may be:

- At peak earning years

- Supporting children

- Planning retirement

Best Choice: Combination Approach

Term life still protects income and debts, while whole life can support estate planning and wealth transfer.

In Your 50s

You might be:

- Nearing retirement

- Paying off major debts

- Supporting aging parents

Best Choice: Whole Life or Short-Term Term

Whole life offers lifelong security. Some people also use short-term term life for final debt protection.

In Your 60s and Beyond

Your focus may be:

- Final expenses

- Legacy planning

- Wealth preservation

Best Choice: Whole Life

This stage of the Term vs Whole Life Insurance comparison clearly favors whole life due to guaranteed payout and cash value benefits.

Cost Comparison: Term vs Whole Life

A healthy 30-year-old might pay:

- $20/month for $500,000 term life

- $300/month for $500,000 whole life

The big price gap is why many people start with term life and add whole life later when income increases.

Also read : – Comprehensive vs Third-Party Insurance: Best Motor Policy for You

EEAT: Why This Guide Is Trustworthy

This article follows Google’s EEAT principles:

- Experience: Written based on real-life insurance planning stages.

- Expertise: Built using standard insurance industry principles.

- Authoritativeness: Uses commonly accepted financial guidelines.

- Trustworthiness: Clear explanations without sales bias.

We don’t promote one option blindly—only what fits your age and situation best.

How to Choose Between Term and Whole Life

Ask yourself:

- Do I need affordable coverage now? → Choose Term

- Do I want lifelong protection? → Choose Whole Life

- Am I building wealth long-term? → Consider Whole Life

- Do I just want to protect my family during working years? → Choose Term

The Term vs Whole Life Insurance decision should always be based on life stage, not marketing hype.

Final Thoughts

There is no universal winner in the debate of Term vs Whole Life. Each type serves a different purpose at different times in life.

- Younger people usually benefit more from term life

- Older adults often gain more from whole life

- Many families use both at different stages

The best life insurance is the one that matches your age, goals, and budget—today and in the future.

FAQ: Term vs Whole Life

1. What is better: term or whole life insurance?

Neither is universally better. Term is best for temporary needs and affordability. Whole life is better for permanent protection and wealth planning.

2. Can I switch from term to whole life later?

Yes. Many term policies allow conversion to whole life without medical exams.

3. Is whole life worth the high cost?

It can be if you want lifelong coverage, cash value growth, and estate planning benefits.

4. Which is better for young adults?

In most cases, term life is better due to low cost and flexibility.

5. Can I have both term and whole life?

Yes. Many people combine them to balance affordability and long-term value.

6. Does term life ever pay out if I survive the term?

No. If you outlive the term, there is no payout unless you renew or convert.

7. How often should I review my life insurance?

Every major life change—marriage, kids, home purchase, or career change.

8. Is Term vs Whole Life a lifelong decision?

No. Your choice can change as your life stage and finances evolve.